The long straddle is a neutral options trading strategy. It is comprised of a long call and a long put, both ATM options . By doing this, traders take positions on both sides of market.

You pay the highest amount of possible premium because you are buying two options, but ATM. For this trade to be profitable, the stock needs to make a move larger than the amount of initial premium paid.

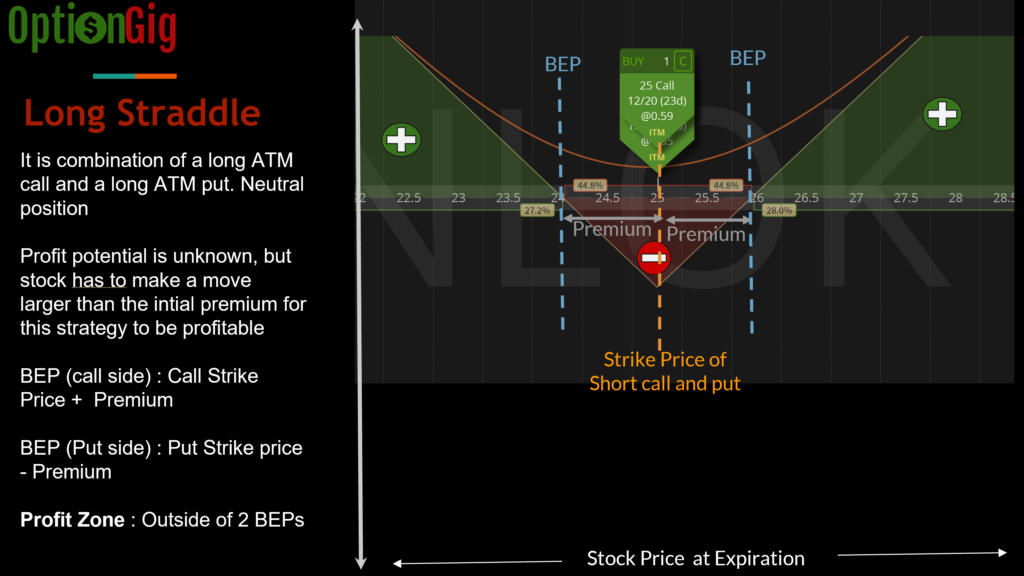

Trade

-Buy 1 ATM call

-Buy 1 ATM put

Trade Example

Stock XYZ is trading at $25.00 a share.

– Buy 25

– Buy 25 put for $0.41

– The total premium paid for this trade is $1.00

Profit & Loss Diagram

Long Straddle Summary

| Break Even Price | Higher side : Strike price of short call + Premium Lower Side : Strike price of short put – Premium |

| Maximum Profit | Unknown. If stock goes to moon, profit would be unlimited |

|---|---|

| Maximum Profit Scenario | Stock either goes to zero or hit the moon |

| Maximum Loss | Amount of initial premium paid |

| Loss Scenario | Stock does not make move or the move is less than the amount of initial premium |

| Why Trade | If you do not have any directional bias in the market , and think that stock can make a huge move in either direction. One scenario where this strategy is popular is near the earnings announcement |

| When to Open | Stock Outlook : Neutral Volatility : Low so you pay less premium to open the trade |

| Which strikes to choose? | There isn’t much option on this. You have to choose the ATM strike |

| When to Close | If the trade is making the desired profit. For me, personally it is one-half of initial premium paid. That’s 50% RoI. |

| Legs | 2 legs |

| Passage of time | Negative impact on trade. With passage of time, the value of this option decreases |

| Increase in volatility | Positive impact on trade. With increase in volatility, the value of option increases. So when you close, you can get higher premium |